Reflationary growth as the base case

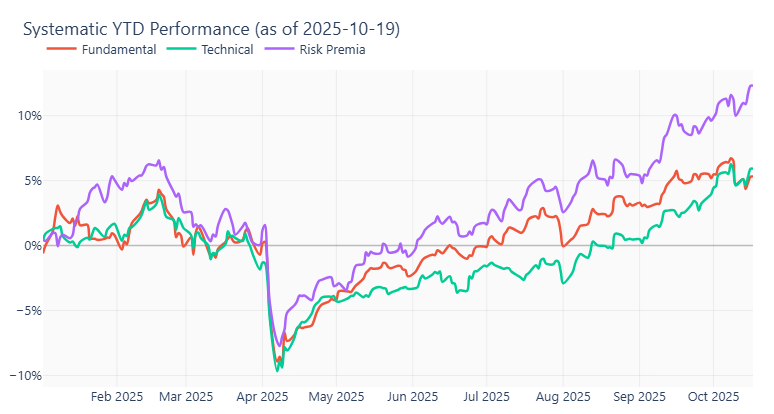

My latest systematic signals are broadly bullish Equities, Metals, Energy, Crypto, Credit, and select EM FX, and are neutral on Rates, Inflation, US Dollar and Agricultural commodities. No broad asset classes are currently showing bearish scores, and individual bearish readings are present in Japanese rates, EUR, NZD and KRW. The opportunity set is not particularly generous at this time, as only a handful of individual markets are showing strong signals. Within equities, South Africa (large exposures to gold and PGM miners), Taiwan (semiconductors/AI revolution beneficiary), and Singapore (relative winner of global trade and tariff wars) are the key bullish picks. Taken together, these signals imply a benign reflationary macroeconomic outlook supported by the AI-related manufacturing boom. As shown in the chart below, my systematic strategy trackers have recovered from the bruising experienced during the Liberation Day crash in April and continue to steadily march higher, with Risk Premia pushing ahead of the Fundamental and Technical themes.

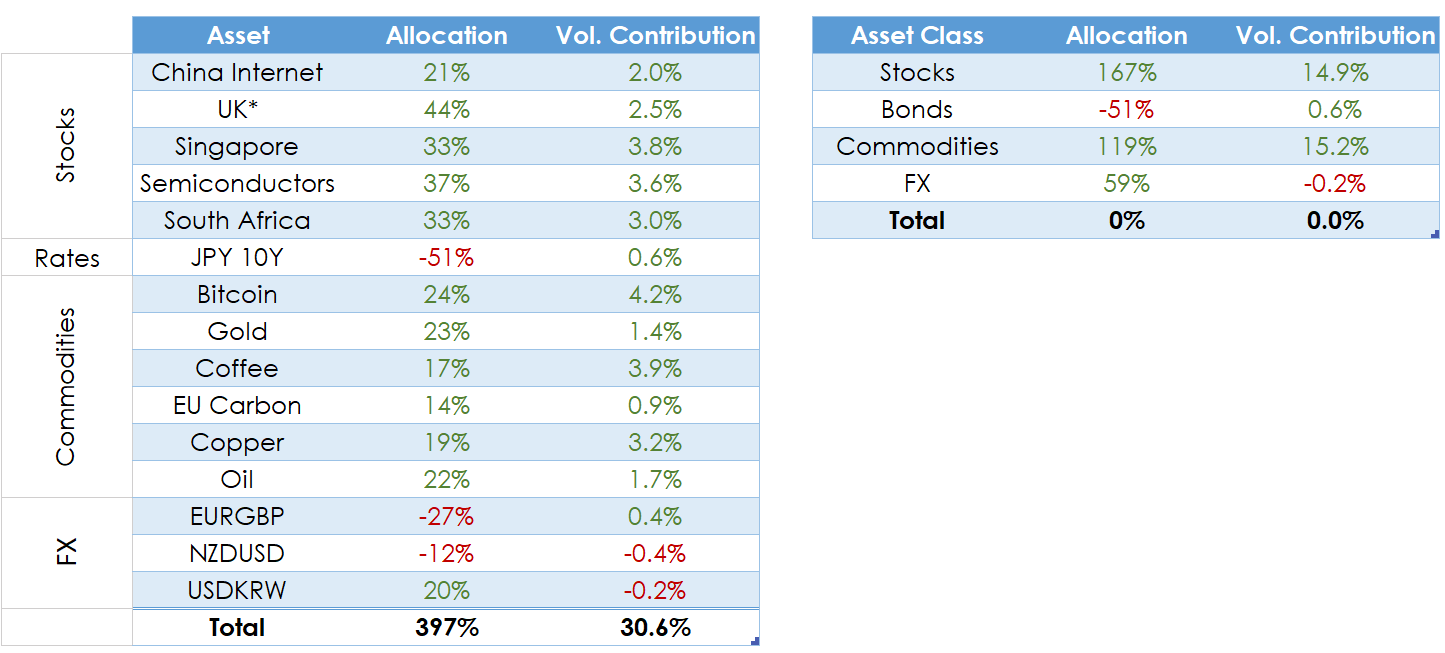

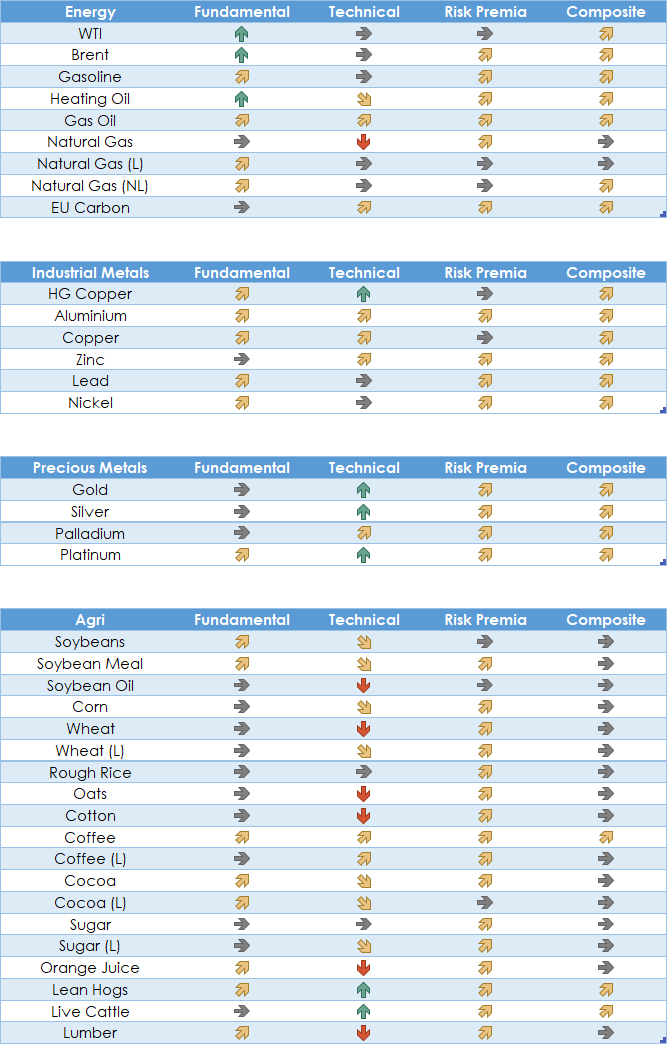

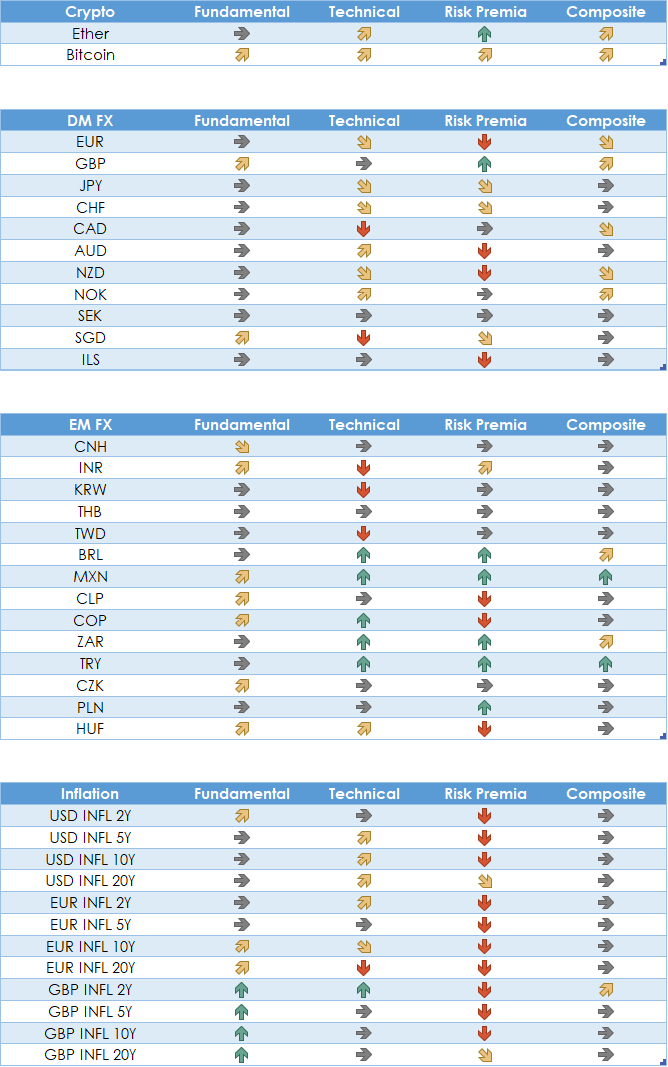

The systematic trackers have around 30 underlying signals across more than 150 markets across the asset classes (full summary in the appendix). My personal investment approach relies on these signals, but is much more focussed, and presently includes 15 distinct high-conviction positions.

Portfolio Positioning

As of Monday 20 October, my key positions are reflation trades (long Commodities, long Equities, short Rates, short EURGBP), Defensive FX trades (short NZDUSD and long USDKRW), and diversifying opportunities in Oil, EU Carbon and Coffee. Today’s allocation and risk contributions are shown below.

*The position in UK stocks is due to be removed in coming weeks.

The rest of this section discusses each of these trades in turn.

1. Reflationary Growth trades: Long Copper, Gold, Bitcoin, China Internet, South Africa, Taiwan; Short 10y JGBs, EURGBP

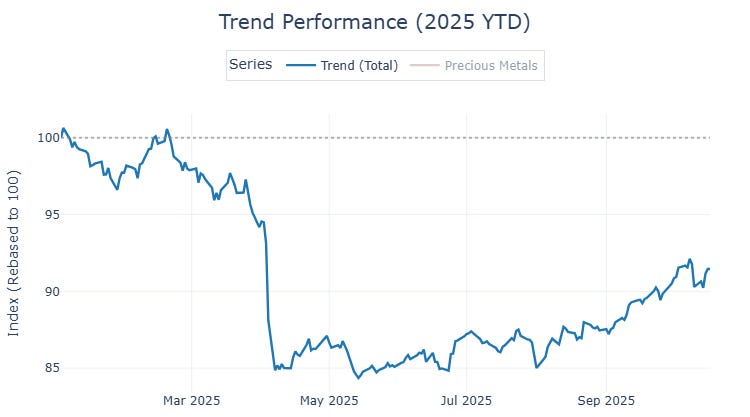

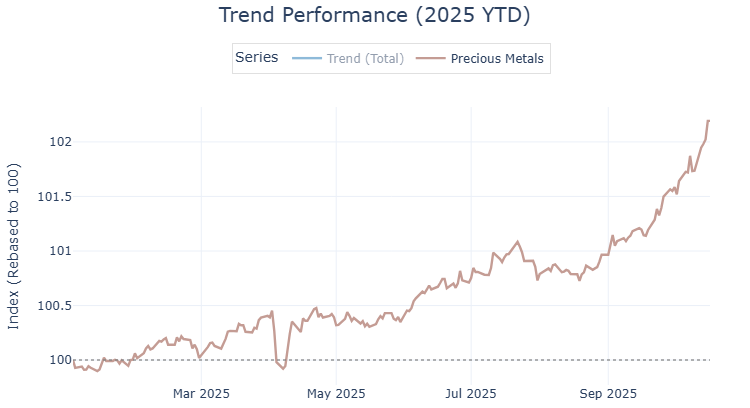

Copper, Gold and Bitcoin have limited and/or inelastic supply, yet presently are facing elevated demand driven by central banking demand, infrastructure demand, and general demand for wealth preservation. With positive economic growth impulse as my base-case, I personally prefer Copper and Bitcoin over Gold. The composite technical score is the highest for US Copper prices, as the 20% tariff-related selloff from late July has reversed only partially thus far. The supply bottlenecks, rising infrastructure demand, and continued trade frictions all point to higher copper prices in coming quarters. Bitcoin has disappointed on a volatility-adjusted basis year-to-date but is potentially facing favourable seasonality in the final quarter of 2025. While Gold continues to show the strongest price momentum across commodities, it appears to be driven more by the de-dollarisation story, which isn’t very consistent with my systematic signal readings in FX. Nevertheless, I keep the allocation to Gold in the portfolio because ignoring price momentum at the time when Trend strategies are recovering very strongly from one of the historically most severe drawdowns earlier this summer, largely thanks to gold and related commodities. For illustration, the top chart below shows the overall performance of my systematic trend strategy, and the bottom chart shows the contribution to trend from Precious Metals sector (Gold, Silver, Platinum and Palladium).

China Internet, South Africa, Semiconductors and Singapore are my top stock market picks. First, China Internet stocks screen as a classic value-plus-catalyst setup: they remain well below their 2021 peaks even after the recent rebound, while mainland inflows and visible AI advances (e.g., competitive LLMs such as DeepSeek) have reignited sentiment, leaving substantial headroom if earnings and policy support keep normalizing. The Beijing authorities appear to have switched priorities from their “common prosperity” objectives to remaining a credible economic challenger to the US. This means that they have now become less uncomfortable with allowing stock market to strengthen, despite its potential to increase the nation’s wealth disparity.

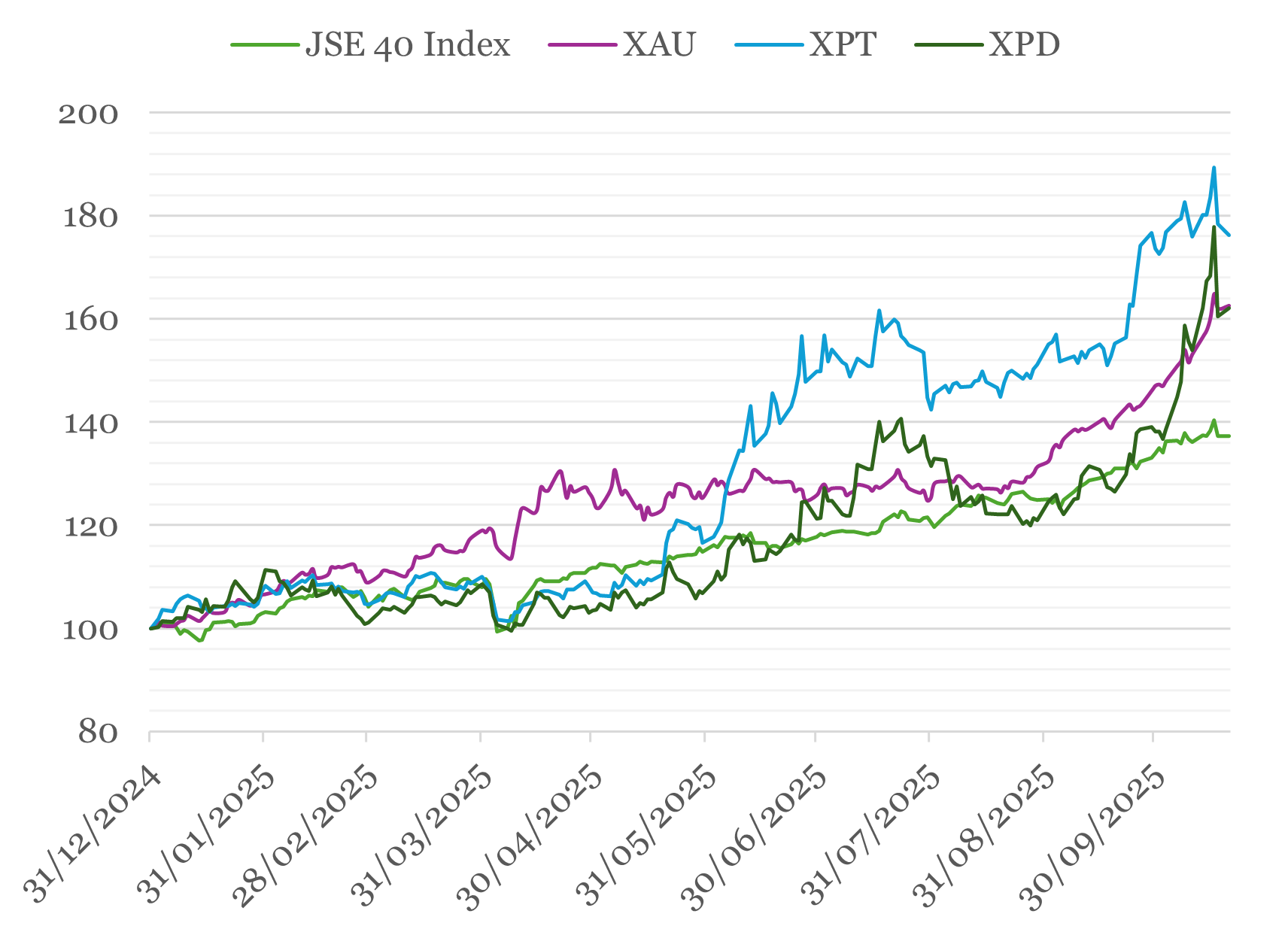

While most signals across developed equity markets are showing positive readings, South Africa, Taiwan and Singapore stand out as the most bullish (green arrows in composite column in the Systematic Signals section at the bottom). It is not difficult to see why. South Africa offers classic leverage to gold and PGMs via hefty Materials weights (~37% of the MSCI Large Cap index) and significant mining sector. As another plus, South African stock market has a strong structural record as one of the world’s best long-run equity performers during its entire history. The chart below shows recent performance of South African stocks alongside some of their key shiny metals, indexed to 100 at the end of last year.

Taiwan is a play on the AI build-out: TSMC produces the vast majority of the world’s most advanced chips and just raised its outlook on “very strong” AI demand; foundry share and profits continue to surge alongside global data-centre CapEx. In an effort to somewhat reduce geopolitical idiosyncratic risk, my preference is to implement this idea via a broader set of global semiconductor stocks. Finally, Singapore is a high-quality, dividend-rich market dominated by local banks that posted record profits through the last cycle. While its banking sectors has become somewhat of a safe haven for global wealth in the last 5+ years, Singapore is also a relative beneficiary of ongoing tariff wars as a key re-export engine, with integrated circuits and electronics trade showing decent momentum. Finally, Singapore’s substantial REITs exposure could benefit as global rates ease in 2026.

Unlike some other macro players, I am not convinced that Japan is facing a significant inflation problem. The soft inflation impulse for Japan is in fact one of the reasons why my short signal for Japanese rates is presently fairly weak. However, I am short 10-year rates in Japan due to technical pressures on monetary policy. The Bank of Japan (BOJ) has for years restrained long-term yields via yield curve control and huge bond buying. Yields have the potential to jump if the BOJ loosens these controls and allow the yield curve to steepen (they have already slowed its buying at the long end of the curve earlier this summer). Finally, I include short EURGBP for additional return potential, a position supported by fundamentals (both growth and inflation prints are running hotter in the UK compared to the eurozone) and favourable technicals (the cross is relatively high in the range, and its YTD momentum is running out of steam).

2. Defensive Positions: Short NZDUSD and long USDKRW.

Whilst I am comfortable with the broad bullish tone of the systematic signals, I seek a disproportionate number of defensive positions in my portfolio. Specifically, I look for positions that directionally align with the systematic signals yet exhibit a negative marginal contribution to overall portfolio risk. For much of 2025, US treasuries had a negative correlation with other major positions, justifying a meaningful allocation in spite of only showing a relatively mild bullish signal. Unfortunately, following the YTD decline of the 10-year rate from 4.57% to 4.00%, that signal now sits very close to zero (neutral).

At this time, the potential diversifiers with meaningful signal strength are short NZD and KRW vs USD. Trend signals are negative for these two currencies due to the sluggish growth in the broader regio. From the risk premia perspective, these currencies exhibit a negative carry vs USD. However, these two are ordinarily pro-growth / risk-on currencies, and as such being able to earn a positive carry from short positions allows us to capture an unusual risk premium while benefitting disproportionately during episodes of market stress and potential crashes.

3. Diversifiers: Oil, EU Carbon, Coffee.

MXN and TRY have very strong bullish signals in my systematic trackers, but these are effectively carry trades, and as such are not helpful when the rest of my portfolio has a heavy stock market exposure. Within FX, I am more comfortable keeping the bullish exposure to USD for downside protection, as explained above. So where do we go for additional and hopefully unrelated return sources?

Oil is presently a bit of a wildcard in the reflationary mix. The current US administration clearly wants to see the prices remain at these levels or weaken further, and they’ve so far been successful through their diplomatic efforts and military actions. That said, traditional fundamental macro signals are supportive of higher oil prices, and oil can continue to act as a tail risk hedge for the specific types of broad market selloffs triggered by any unanticipated geopolitical tensions in key regions, making the long position valuable in the portfolio context.

Long EU Carbon emissions a structural position benefitting from the persistent supply squeeze in the market driven by the powerful regulatory effort to address the challenges related to climate change. My personal insights into the nuances of this market are limited, but the systematic signals I follow have been historically profitable and presently point to a continuation of the recent bullish direction.

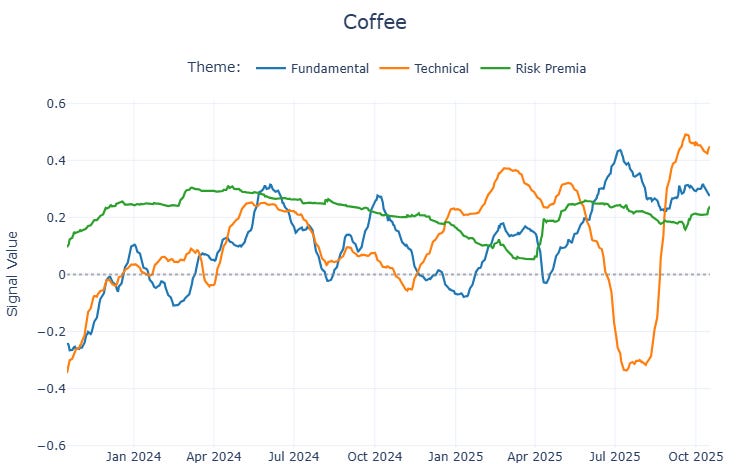

Coffee’s bull case rests on continued supply tightness, low exchange stocks, weather risk, and policy frictions, which are very difficult to track and evaluate due to Coffee’s globally diversified supply base. My inputs for this market are for the most part technical, and related to price momentum, distributional reversals, and anomalies exploitable from the shape and movements of the futures curve. As seen in chart below, non-technical themes (fundamentals and risk premia) are also presently bullish, adding to the technical conviction from the systematic perspective. Due to its relatively weak correlation with core positions, I expect a modest allocation to Coffee to be a valuable distinct source of potential additional returns.

I will be sharing more details about the underlying signals, strategies and themes in the future.

The Week Ahead

The FOMC is entering its blackout period this week, ahead of their October meeting next week, but there is a good lineup of ECB speakers this week. The earnings season in the US is picking up, with Tesla, IBM and Barclays reporting on Wednesday. meeting. UK inflation figures are also coming out on Wednesday, and the BLS will be releasing the delayed September inflation figures for the US on Friday. Some of the key events I will be following this week are:

Tuesday, October 21:

ECB’s Lagarde, Lane, Nagel and Kocher speak

Wednesday, October 22:

UK CPI / RPI / PPI

South Africa CPI

ECB’s Lagarde speaks

Earnings: Barclays, Tesla, IBM

Thursday, October 23:

BOK Base Rate decision

ECB’s Lane speaks

Turkey Repo rate decision

SARB monetary policy review

US claims, existing home sales, Chicago Fed activity,

Friday, October 24:

Eurozone HCOB PMIs

ECB’s Nagel and Villeroy speak

US CPI (delayed), S&P PMIs, new home sales, Michigan sentiment

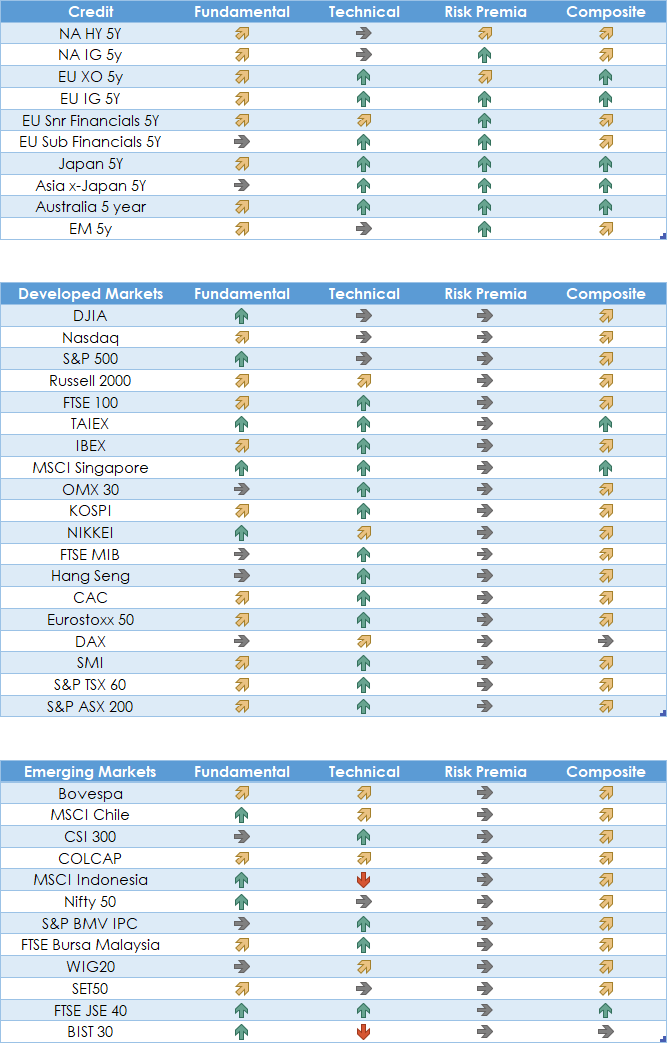

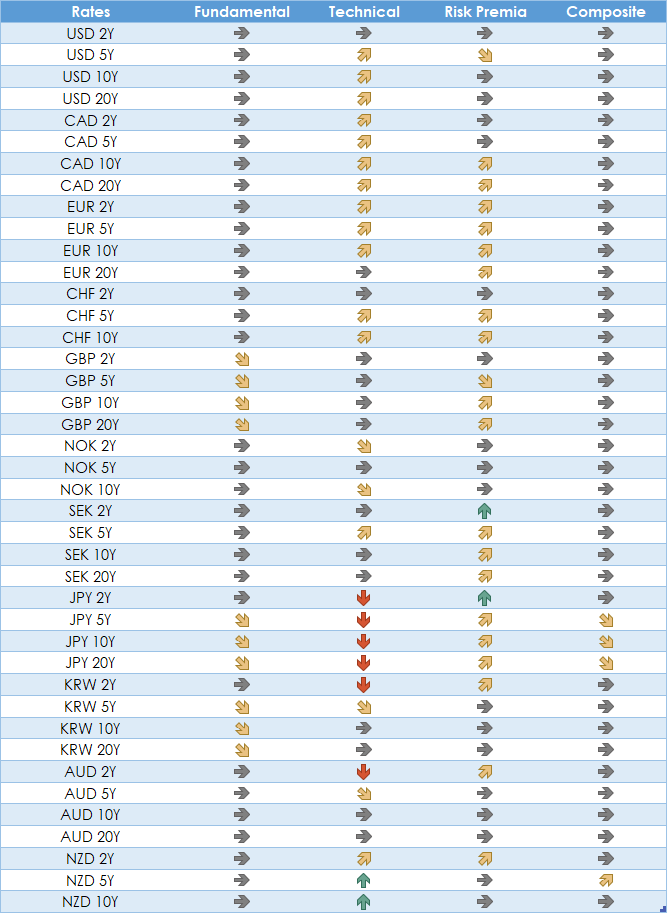

Systematic Signals

Disclaimer

I do not provide dealing, solicitation, or advisory services in futures or securities, and I do not offer asset management services. All publications are made available to the public. My personal allocations and opinions are provided for educational purposes only, are not tailored to any specific reader, and do not constitute investment advice.