Executive Summary

I increased my short 10-year JGB exposure from -53% to -98% on Friday because I see Japan transitioning from policy-anchored yields to renewed price discovery, reinforced by wage-driven inflation dynamics and a more political/fiscal backdrop. Policy backstops, FX intervention spillovers, and sharp safe-haven rallies remain key risks to this thesis.

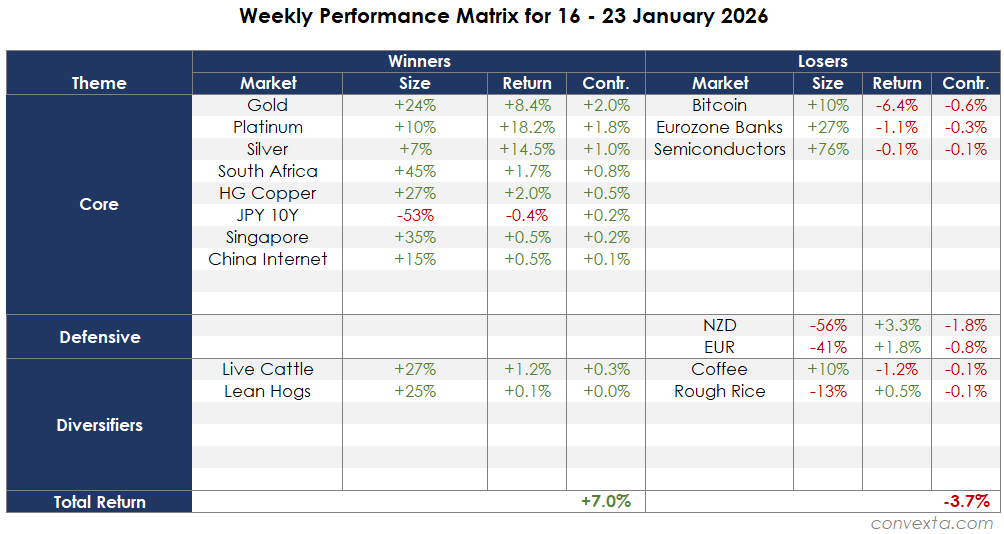

My macro strategy had a strong week, led by precious metals. On a Friday close-to-close basis, the model return was +3.3%, driven primarily by gold, platinum, and silver, with additional support from South Africa and copper. The main drags were short NZD and short EUR as USD failed to behave as a defensive hedge.

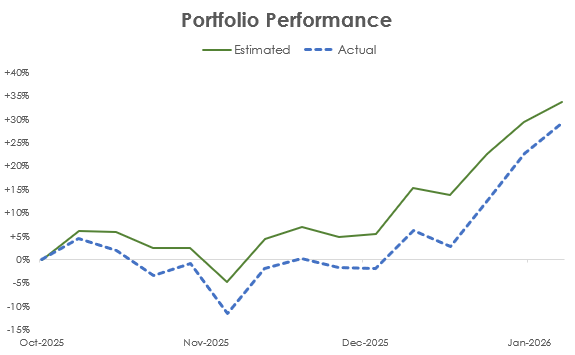

My actual portfolio returned +5.4% last week, about +2.1% above the weekly model estimate, mainly from additional tactical trades: the TACO risk trade into DJT’s speech, re-entering EUAs on the dip, and adding to my short 10-year JGB position on BOJ Friday. The cumulative gap between model and realised performance continues to narrow since I tightened execution and risk management.

Why I’m Adding to Short JGBs

As flagged in my live chat, I increased my short 10-year JGB exposure from -53% to -98% on Friday, following the mid-week reversal in yields from c.2.35% to c.2.23%. In risk terms, this position now contributes 1.9% volatility my 41.6% vol portfolio, which makes it a meaningful, but still well-controlled expression within the broader book.

What followed was BOJ Governor Ueda’s press conference, Prime Minister Takaichi’s escalated rhetoric about acting against “speculative” market moves, and Finance Minister Katayama reinforcing the messaging around intervention being an option.

Intervention threats are certainly a risk factor, but they are mainly directed at the FX market, not bonds. I think the authorities are genuinely trying to smooth volatility around a regime shift they can’t easily reverse. Japan is moving from a world of controlled rates into a world where the bond market is re-asserting price discovery.

1. Inflation is now seen as wage-driven, not imported

The decision to hold the policy rate at 0.75% was widely expected. The important part of Ueda’s messaging was the emphasis that

the BOJ believes the economy is in a moderate recovery,

wage growth is becoming a durable inflation channel, and

the BOJ intends to continue normalising if its forecasts play out.

Ueda explicitly noted that where inflation had previously been driven by raw materials, labour costs are now a key driver. This is a crucial distinction, because it’s the type of inflation that central banks treat as persistent.

Even more important: Ueda signalled he doesn’t want to be held back by slow-moving hard data, and that the BOJ will also look at faster information such as corporate surveys when making timely decisions. That to me sounds like he is trying to keep optionality to keep hiking while inflation psychology is live.

My base case remains that the market is still underestimating how far the normalisation process can go, especially once the bond market begins to demand a proper term premium again.

2. The catalyst has become political

The violent repricing in JGBs has recently taken on political drivers. Takaichi’s snap election call and her stimulus/tax relief campaign has forced investors to re-price fiscal risk into long rates. Buyers have stepped back from Japanese debt as the campaign turns into competitive spending promises, and yields surged at a pace not seen since prior stress episodes.

This weekend’s intervention rhetoric reinforces that policymakers are now juggling an unstable triangle: a weak yen feeding inflation, bond yields rising as fiscal concerns mount, and a central bank that wants to normalise without triggering disorderly market dynamics.

This weekend, Takaichi vowed to act against speculative market moves, while her own fiscal agenda (including a large spending package and a planned suspension of the food sales tax) is part of what aggravated the bond selloff in the first place.

When fiscal credibility becomes a first-order variable, the bond market doesn’t need a lot of “bad news” to continue to slide. It just needs uncertainty, and an election campaign is uncertain by design.

3. Intervention is a risk, but the focus is on volatility

I’m taking the intervention threats seriously, but I believe I am interpreting them correctly. The loudest weekend rhetoric is primarily about FX market stability, not about a new yield cap. On Friday, Katayama said she was watching FX closely and declined to comment on speculation about “rate checks,” a classic precursor theme in intervention narratives.

In bond space, Katayama’s tone has been to calm the markets (and, per reporting, to suggest the acute phase of the rout had receded), while Ueda explicitly resisted declaring the selloff over, saying volatility remains high and he wants to scrutinise developments carefully.

That divergence tells me the government wants stability, while the BOJ is not promising a backstop. They seem comfortable with a continued repricing of the yield curve, as long as it remains relatively gradual. The BOJ is not running hard yield-curve control, and verbal intervention may be effective at changing the speed of the move more than the direction.

4. The BOJ toolkit is real - and it defines the risk I’m taking

Japan has a number of options. The BOJ can slow bond-purchase tapering further, conduct emergency bond buying operations, and coordinate with the government on market functioning. The government can also adjust issuance or consider buybacks.

But they are likely to only use these primarily as volatility-control tools. Such steps may help stabilise markets temporarily, but they don’t solve the underlying forces pushing yields up, especially if fiscal policy is leaning expansionary into an election.

The BOJ is trapped between a) inflation dynamics that they believe justify further hikes and b) political realities that make it hard to commit to aggressive, persistent bond-buying again without damaging credibility. In this environment, long-dated rates can keep repricing higher.

Why size up now?

Ueda’s press conference effectively told us that the normalisation process continues, rather than that yields should be controlled or capped at a certain level. The weekend commentary added a second layer: officials are now publicly signalling concern about speculative moves, which tends to happen after a regime has already shifted.

That combination reinforces the structural bear case and makes me want the short to be a core position rather than a tactical one. The timing may not be ideal, but 1.9% risk contribution is far from excessive. I am willing to tolerate noise because I think the yen will be the key intervention target, and the big picture move is the market is forcing Japan’s long end to behave like a normal developed market again.

How far can this trade go?

The 10-year JGB yield has pushed above 2.2%, a 27-year high, and 2025 has already delivered the steepest annual rise in benchmark JGB yields since 1994. In price terms, front-month 10-year JGB futures are roughly 8.2% below their 2019 peak.

The closest modern analogue is the US inflation shock: between August 2020 and October 2022, US 10-year yields rose from 0.52% to 4.29%, and 10-year Treasury futures suffered a drawdown of more than 23%, the worst on record. Relative to that episode, Japan’s duration adjustment still looks incomplete.

Japan’s own history argues that much deeper drawdowns are possible when the BOJ tightens into inflation. During the late-1980s inflation cycle, the BOJ began hiking in May 1989 and raised rates five times within eight months, taking the policy rate to 6% by August 1990. In that regime, long-dated JGBs lost more than 20%, as term premia repriced sharply higher. That episode is a reminder that Japan is not immune to large bond bear markets when inflation and policy tightening reinforce each other.

Key risks and mitigation measures

Short JGBs is the classic “widowmaker trade”. Here are the key risks that matter today:

Policy shock risk: If the BOJ signals a de facto yield backstop (or materially expands purchases) rather than just warning about disorderly moves, JGBs can rally violently.

FX intervention / risk-off squeeze: If yen intervention triggers a broader de-leveraging and a global duration grab, JGBs can rally even if Japan’s medium-term story is unchanged.

Political reversal risk: If fiscal proposals are toned down, or if the election narrative pivots toward restraint, term premium can compress.

Crowding / positioning: When the market becomes convinced of “one direction,” squeezes become larger and more frequent.

Broad risk-off: JGBs rallied sharply during the August 2024 growth scare and during April 2025 liberation day crash. In acute risk-off episodes, JGBs can still trade as a safe haven, which is adverse to my short.

My risk mitigation measures are as follows: I’m keeping the position in the most liquid part of the curve (10Y), I’m sizing it as 1.9% vol within a ~41.6% vol portfolio, and I’m willing to adjust tactically around BOJ-driven volatility without dropping the structural direction.

This is not a bet that Japan will implode next week. It’s a bet that the market has entered a new regime where the cocktail of questioned fiscal credibility, inflation persistence, and BOJ normalisation will keep demanding higher yields over time.

Market Backdrop and Portfolio Performance (16 - 23 Jan)

The most significant market development during last week was weakening of USD, hit by the toxic cocktail of Greenland and tariff brinkmanship colliding with Davos messaging. The uncertainty and reaction that these diplomatic / political manoeuvres generated hit confidence in US policy coherence and triggered a sharp USD drawdown.

The dollar had its steepest weekly drop in months, while investors piled into hard-asset safe havens: gold logged its best week since 2008 (up more than 8%) and silver punched through $100. In parallel, risk assets were choppy rather than outright collapsing.

US equities had a relief rally on Wednesday and stabilized into Friday, but idiosyncratic tech weakness (notably Intel) weighed on the “growth” complex, while Europe lagged as the STOXX 600 snapped a winning streak amid renewed trade jitters and softer-than-expected eurozone activity momentum.

Portfolio performance

On a Friday close-to-close basis, using the published end-of-week allocations and assuming no intra-week adjustments, the performance matrix implies +3.3% for the week (gross winners +7.0% offset by -3.7% for losing positions). The P&L was heavily led by precious metals, with a smaller positive tail from industrial metals and rates, while FX and crypto were the main headwinds.

In my core theme, the key contributors were Gold (+2.0% contribution), Platinum (+1.8%), and Silver (+1.0%). South Africa (+0.8%) added as the mining-linked beta participated in the same hard-asset impulse, and Copper (+0.5%) contributed despite lagging behind its shinier siblings.

The short JPY 10Y position also helped (+0.2%) as Japanese rates continue to price the BOJ as falling behind the curve into their monetary policy meeting towards the end of the workweek. Smaller positives in Singapore (+0.2%) and China Internet (+0.1%) were incremental rather than central to the story, but they helped round out the week.

The offsets were cleanly concentrated. Short NZD (-1.8%) and short EUR (-0.8%) were the main drags. The USD did not play its intended defensive role in the selloff that was driven by concerns around United States’ credibility and reliability. Across my diversifiers, Live Cattle (+0.3%) was a positive contributor, while Coffee (-0.1%) and Rough Rice (-0.1%) were marginally negative for the overall performance.

Tactical trades added further +2.1%

My actual portfolio return for the week was +5.4%, outperforming the close-to-close “model” estimate, by c. +2.1%. This additional performance is attributable to tactical trades that were discussed in my Live Chat, most importantly:

the TACO trade (leaning long risk into DJT’s speech),

re-entering EUAs (Dec 2026 contract) on the dip, and

adding to short JGBs on BOJ Friday.

Zooming out, last week brought my cumulative actual performance to 29.4%, and my model performance to 33.6% since the launch of my newsletter in late October.

The cumulative gap between “model” and realised performance has continued to narrow since I identified the underlying issues and introduced a more active trading and risk-management process at the turn of the year. As laid out in Three Months In: Strong Start. Bar Raised., the key upgrades have been:

actively offsetting leveraged-ETF rebalance/volatility drag with derivatives and rebalancing when exposures drift,

reducing proxy reliance and using more conservative betas where proxies remain,

cutting costs by consolidating accounts/brokers where possible,

tightening tactical trading to setups with a demonstrable intra-week edge, anchored by a clearer ruleset around execution and position management.

Without getting into the specifics at this time, there is further room for improvement on points 2, 3 and 4. These remain ongoing to-dos.

Positioning and Trading Plan

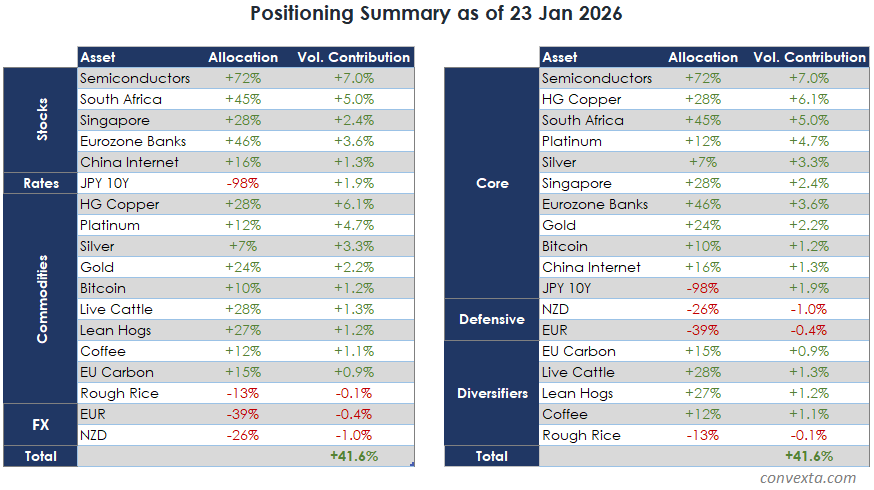

Last week saw three significant changes in my positioning, discussed in my Live Chat during the week:

Doubling down on JGBs on Friday (from -53% a week ago to -98%),

re-entering EU Carbon with 15% exposure on Wednesday, and

cutting NZD shorts from -56% to -26% during Friday.

The table above shows my portfolio across the asset classes (left) and across my key macro themes (right). The methodology behind allocations and volatility contribution is explained in my Foundations piece Asset Allocation is Dead. Long Live Asset Allocation!

The overall structure remains unchanged: Core positions across broad growth and selective reflation first, Diversifiers second, with Defensives acting as a modest counterweight. For a more comprehensive explanation of my portfolio, please revisit Positioning for Reflationary Growth.

Total portfolio volatility sits slightly above the 40% strategic target, and the risk budget is concentrated in the Growth engine. I feel comfortable running the engine slightly hot when I am in the green. The highest volatility contributions are coming from equities (+19.3%, with Semis the most significant contributor at +7.0%) and metals (+16.3%, dominated by copper). Of course, one could argue that the +5.0% risk contribution from South Africa belongs to the metals bucket, in which case the primary risk factors in my portfolio come from metals, not the stock market.

My key trading priorities are listed below:

Explore ways to furtherdiversify beta exposure, an expression of the broadening growth theme.✅Complete, EZ Banks addedRe-evaluate the risk of intervention threats for JGB short positions and adjust the exposure accordingly.

Re-evaluate the relevance of long USD as a defensive play and look for alternative defensive allocations.

Key Catalysts Next Week (Mon 26 Jan - Fri 30 Jan)

The coming week will be data-heavy. The week sets up as a four-way tug of war between US macro/FOMC (USD and rates impulse), AI/mega-cap earnings (semis risk appetite), North Asia / Europe data (Japan CPI/BOJ minutes, Eurozone GDP/CPI), and Washington shutdown brinkmanship, which could inject headline-driven volatility and risk-off squeezes even if the data prints are benign.

Monday, 26 Jan

Germany IFO business climate. Important for Europe growth tone and my Eurozone Banks / short EUR exposure.

Singapore industrial production. Direct relevance for my Singapore exposure and broader Asia cycle tone.

US durable goods + Dallas Fed manufacturing. Second-order input into the US growth pulse that the market will carry into FOMC week.

ECB’s Nagel speaks. Potential EUR/banks narrative risk if it shifts the expected ECB path.

Tuesday, 27 Jan

China industrial profits. Relevant for global cycle tone and directly for China Internet, indirectly for Semis / Copper.

US consumer confidence + Richmond Fed. Sentiment/activity pulse heading into Wednesday.

EU-India summit. Potential headline generator for risk tone.

US Paris Agreement withdrawal. Narrative catalyst that could influence Europe’s policy stance and market expectations around EU carbon emissions.

Wednesday, 28 Jan

FOMC rate decision + Powell press conference. The central risk event for USD, rates, and risk appetite. No rate change is expected, and because this is a non-SEP meeting (no new dots/forecasts), the entire event is about Powell’s press conference and the reaction function it signals.

Australia CPI + Canada rate decision + Brazil rate decision. Global inflation/policy cluster that can widen FX/rates outcomes.

Earnings: Meta, Microsoft, Tesla, ASML. AI capex / guidance reality check for my Semiconductors exposure.

BOJ minutes. Direct relevance for my JGB short.

Thursday, 29 Jan

South Africa rate decision + PPI. Direct relevance for my JSE Top 40 exposure.

New Zealand trade + ANZ business confidence. Direct relevance for my NZD short.

Singapore unemployment. Local macro pulse for Singapore exposure.

US jobless claims + macro cluster. Second major US pulse after FOMC.

Earnings: Apple + Deutsche Bank. Risk tone marker (Apple) and a clean catalyst for Eurozone Banks.

Friday, 30 Jan

Eurozone GDP + unemployment + ECB inflation expectations; Germany CPI/GDP/unemployment. High relevance for Eurozone Banks and EUR.

Japan Tokyo CPI + jobs + industrial production + retail sales. Key macro set for my JPY 10Y short.

South Korea industrial production + Taiwan GDP. Important for North Asia cycle tone and indirectly for Semis.

US PPI + Chicago PMI. Final US inflation/growth pulse into month-end.

US federal government funding deadline. Multiple US senators said they would vote against upcoming government spending bills after federal agents killed an American citizen in Minneapolis, significantly increasing the chances of a government shutdown.

Ongoing risks without fixed timestamps

US/DC headlines: Even though the funding deadline is on Friday, the renewed shutdown risk can dominate headlines throughout the entire week.

Japan intervention risk: Prime Minister Sanae Takaichi warned of action on abnormal currency moves, and traders will start the week on heightened alert of Japanese government intervention to halt the yen’s recent slide, possibly with rare US assistance.

Disclaimer

Convexta does not provide dealing, solicitation, or advisory services in futures or securities, and does not offer asset management services. All publications are made available to the public. Authors’ personal allocations and opinions are provided for educational purposes only, are not tailored to any specific reader, and do not constitute investment advice.

Good evening