Markets had a tantrum last week, selling off hard despite fundamentals moving in favour of risk assets. Earnings remained firm, labour-market cooling continued, and inflation data turned softer all reinforcing my non-consensus call for a December Fed cut. Yet global stock markets continued their sell-off in a catalyst-free, flow-driven shakeout that said more about positioning stress than macro reality.

My macro indicators continue to support my headline growth thesis; Japan’s fiscal splash hasn’t derailed the reflationary setup; and China’s policy rumour-mill has turned more active just as tech earnings stabilise. Metals remain in consolidation, rather than reversal of the bullish trend.

It was a rough tape, and my book took a hit, but defensive FX and duration cushioned part of the blow. With fundamentals improving and technicals still supportive, I remain positioned for stabilisation, with a tighter risk-management stance into year-end.

Rebel Without a (Macro) Cause: When Markets Throw Tantrums

Last week’s earnings releases have been resilient, labour-market cooling continued at a controlled pace, and inflation indicators have leaned soft. The underlying growth picture is supportive for the long positions in equities, and the pillars that matter for the coming Fed meeting - labour slack and price moderation - are tilting in the direction of my call for a December rate cut.

Yet markets traded as if the opposite were happening. The S&P500 futures closed c. 4.5% below their all-time-high in a disorderly, sentiment-driven move, without a discernible catalyst - a reminder that the stock market and the economy are two different beasts. The selloff in high-beta assets, the rotation away from growth, and the impulsive swings across commodities speak more to positioning stress and risk-management flows than to any shift in macro momentum.

It reminded me of Rebel Without a Cause: like James Dean’s character, the market is lashing out in dramatic, directionless bursts - not because anything fundamental changed, but because of the internal tensions it carries around. Flows can trigger surges in volatility even when the signal remains intact, and this is when maintaining thematic conviction matters more than reacting to every downdraft.

U.S.: The Case for a December Cut Keeps Firming

If last week had a single macro message, it was this: inflation remains high without accelerating, labour-market cooling is real, and the December Fed cut is more plausible than the market is willing to acknowledge.

The delayed September Employment Situation painted a mixed picture: 119k jobs were added to payrolls, but the unemployment rate nudged higher, from 4.3% in August to 4.4% in September.

U.S. Import Prices for October landed at 0.0% m/m, in line with consensus and consistent with softening traded-goods inflation. This keeps the inflation component of the Macro Pulse signal in the comfortably negative range: inflation surprises are likely skewing to the downside, even if headline levels remain slightly above target.

This is precisely the kind of environment that gives the Fed political and analytical air cover to cut. Labour demand is cooling in a way that reduces any credible risk of overheating. A meaningful part of the labour-market softness appears to be AI-driven and structural rather than cyclical, and inflation continues to deliver soft surprises that chip away at fears of persistence.

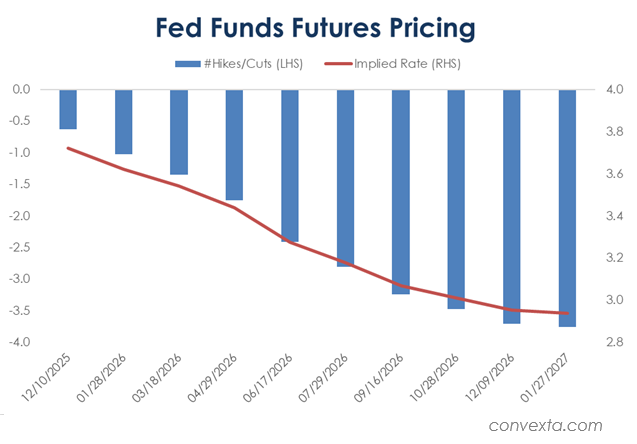

Taken together, the combination weakens the case for staying restrictive and strengthens the argument that the balance of risks across both mandates is shifting in favour of easing. Friday morning’s dovish comments by John Williams (NY Fed President) had a visible impact: at the week’s close, Fed Funds Futures were pricing a 63% chance of a cut at the next meeting, up from 43% a week earlier.

The December Cut Checklist

Below is the updated tracker of key data points that should encourage the FOMC to pivot towards cutting on 10 December, originally outlined in the last Weekly Macro Playbook Metal Mayhem: Enter the Mosh Pit.

Released:

Tue 18 Nov: U.S. Import Price Index (Oct)

✅ Dovish: 0.0% MoM, in line with expectations,Wed 19 Nov: Employment Situation (Sep, delayed)

✅Dovish: Unemployment rate increased to 4.4% vs. 4.3% median estimate

Forthcoming:

Tue 25 Nov: PPI Final Demand (Oct)

Economist estimates are centred around 0.3% MoM. A softer print would marginally increase the odds of a December cut.Wed 26 Nov: Personal Income & Outlays (Oct) incl. PCE Price Index

The Fed’s preferred inflation gauge. The September reading was soft before the shutdown; another modest print here would materially shift the December debate.Mon 1 Dec: ISM Manufacturing (incl. Prices Paid)

Prices Paid has been declining since June this year. A further cooling should reinforce the idea that pipeline inflation pressure is fading.Fri 5 Dec: Employment Situation (Nov)

The full monthly jobs report - the second most important dataset ahead of the December meeting.Wed 10 Dec: CPI (Nov) at 8:30 ET

The single most consequential release of the next month. The FOMC statement and press conference follow later the same day.

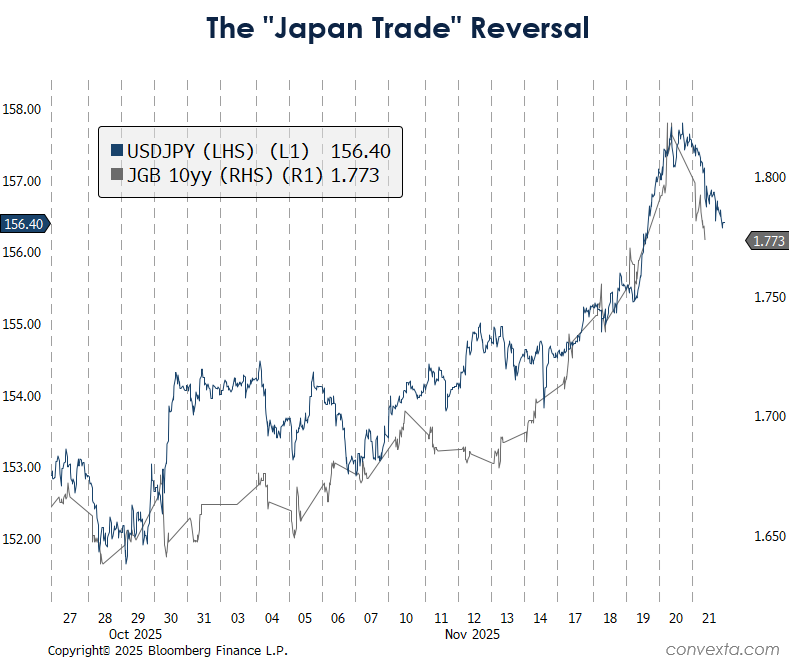

Market Shrugs to Japan’s Fiscal Big Bang

Japan delivered its largest fiscal package since the pandemic: a ¥21.3 trillion programme aimed at cushioning households from rising living costs. Roughly ¥11.7 trillion is dedicated to near-term relief: household subsidies, a ¥20,000 child allowance, lower energy bills and the scrapping of the gasoline tax. Government estimates suggest the measures could trim inflation by about 0.7pp for several months and lift GDP by roughly 1.4% per year over the next three years.

Market reaction was sobering. The 10-year JGB yield dropped about 3bp and JPY strengthened around 0.5%, following a 20bp sell-off in JGBs and a c. 4.5% yen drop over the past month. It felt like a “buy the rumour, sell the fact” moment.

Regardless, the fiscal stimulus will at best relieve the impact of higher prices on households in the near-term, while leaving underlying inflationary pressures unaffected. That combination should delay inflation, not defeat it.

The Nationwide CPI printed 3.0% y/y on Friday, in line with expectations, and the rate hike probability for December declined from 32% last week to 22% at the end of the week.

For markets, this keeps the existing themes in place. The yen remains biased weaker in the absence of BOJ tightening, though intervention risk has risen: Finance Minister Katayama was explicit this week about the need for FX stability. The curve-steepening story also remains in place, supported by rising structural spending on defence, social security and economic security, even if the pace is glacial. And inflation risks remain asymmetric, not less: the package supports spending but does little to expand supply.

In portfolio terms, the conclusion is unchanged. Short JGBs and JPY positions continue to express the reflationary potential from the policy mix, but sizing reflects the lack of obvious near-term catalysts.

China: Macro Fear Meets Policy Hope

Last week saw a number of earnings reports from Chinese tech companies. Trip.com delivered another robust beat on travel demand, Xiaomi posted impressive top-line and EV-driven profit growth, and Kuaishou’s operational momentum remained solid - all consistent with a normalisation in China’s consumption and services economy.

In contrast, Baidu’s ad-revenue decline and NetEase’s cautious commentary overshadowed otherwise respectable prints, reinforcing concerns that China’s legacy internet cycle is still in a low-energy phase.

The result was a market that largely shrugged off the positives and traded more on macro unease and positioning stress, rather than company fundamentals. The broader market tone remained heavy and China Internet stocks declined by 4.7% during the week, in concert with the global weakness in tech names.

No major hard data prints came out of China last week, but the policy rumour mill was unusually active. A Bloomberg report suggested that Beijing is weighing a fresh round of property-support measures as authorities grow increasingly uneasy about the sector’s drag on growth and its role in amplifying deflationary pressures. The ideas reportedly on the table range from broader mortgage incentives to tweaks in transaction taxes and rebates - incremental tools rather than a 2009-style bazooka, but meaningful in signalling intent.

None of this is confirmed, but the direction of travel matters: discussion of targeted housing support is entirely consistent with the thesis behind my China positioning. The bull case is the potential for a reversal driven by a policy catalyst. The renewed noise around stabilisation efforts fits squarely into that framework.

UK: CPI deceleration Reinforces BoE Easing Path

The UK CPI release for October came in a notch hotter than the median economist estimate: 3.6% vs 3.5% y/y. In spite of the positive surprise and elevated level, the deceleration from previous months largely cements the December BoE cut as the base case (now c. 88% priced). My EURGBP short is mainly a relative inflation pressures play on monetary policy path, has delivered a positive return during the week.

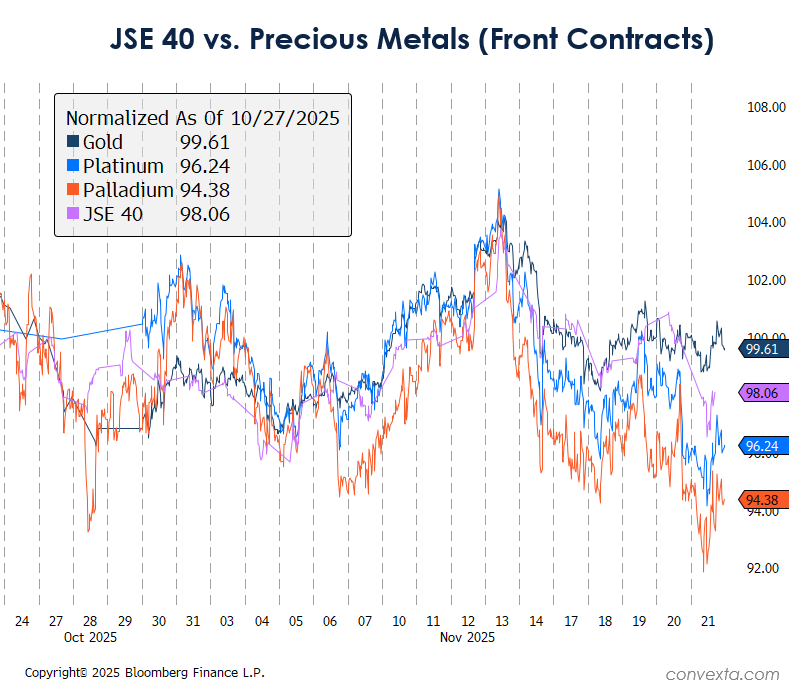

Metals Range-Bound, Outlook Intact

South Africa’s macro data last week did not alter the investment landscape. The CPI rate increased from 3.4% y/y in Sep to 3.6% y/yin October. With the official inflation target now at 3% with the +/-1% tolerance band, the SARB cut rates by 25bps to 6.75%, noting that the inflation outlook had improved enough for policy to become less restrictive.

Gold prices remained correlated with the stock market, but range-bound during the week with less downside. Higher-beta metals like Silver, Platinum and Palladium slightly underperformed gold, while copper was down the most, around 0.8% on the week. As metals continue to consolidate, my bullish outlook remains unchanged from my recent update in Heavy Metal Meltdown: Why the Music Stopped, and why the Encore Could Be Explosive.

Performance Review: The Shakeout Week

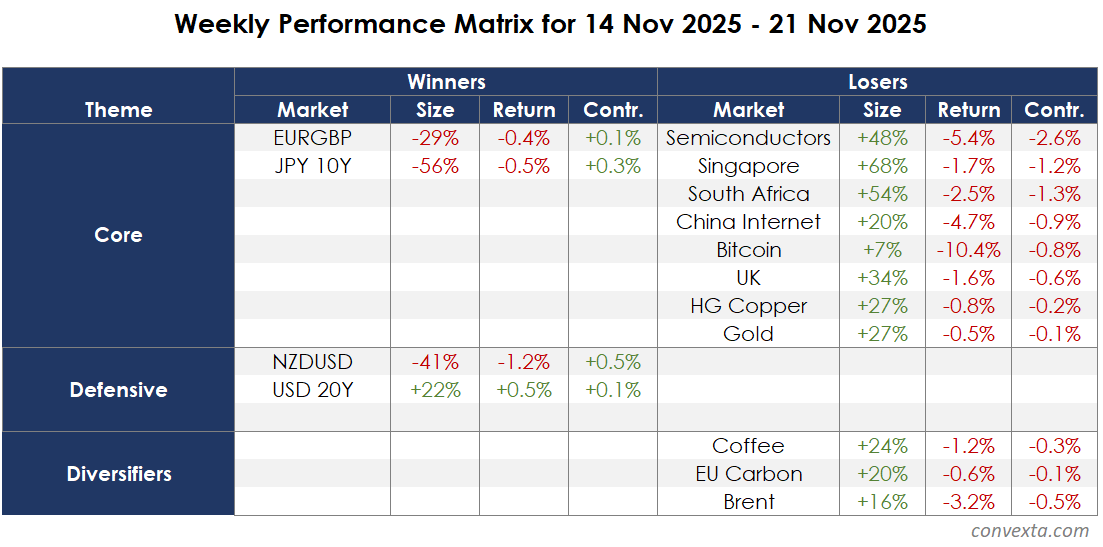

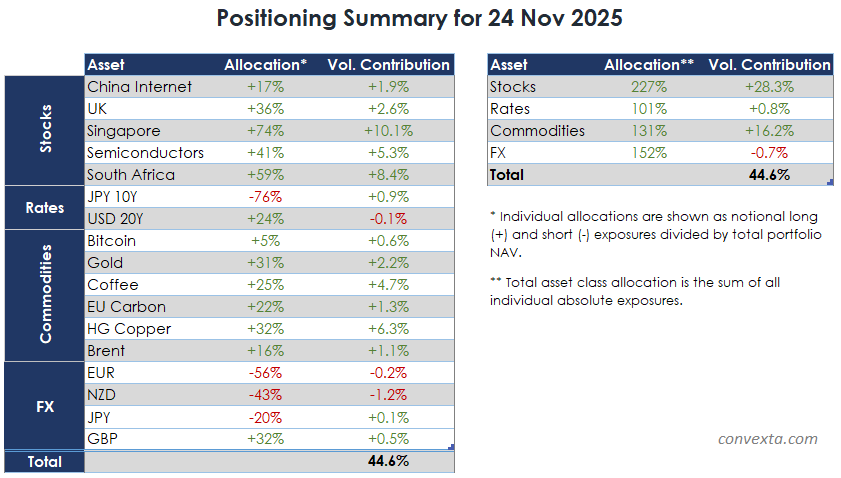

The week was defined by a broad de-risking across global equities and commodities, which hit most positions in my Core and Diversifier books. Short positions in JGBs, EURGBP, and NZD, as well as the longs in Ultras (20y USD bond futures) were the only offsets. The overall loss was around 7.7% for the week.

Long Semis was the largest loser, reducing the portfolio NAV by c. 2.6%, followed by MSCI Singapore (-1.2%), JSE40 (1.3%) and China Internet stocks (-0.9%). Bitcoin continued to lead the declines, dropping more than 10% on the week to sub-85k levels - a strong support zone. However, the damage to the portfolio was limited to 0.8% as the exposure had been cut from c. 24% on 20 Oct to c. 7% a week ago.

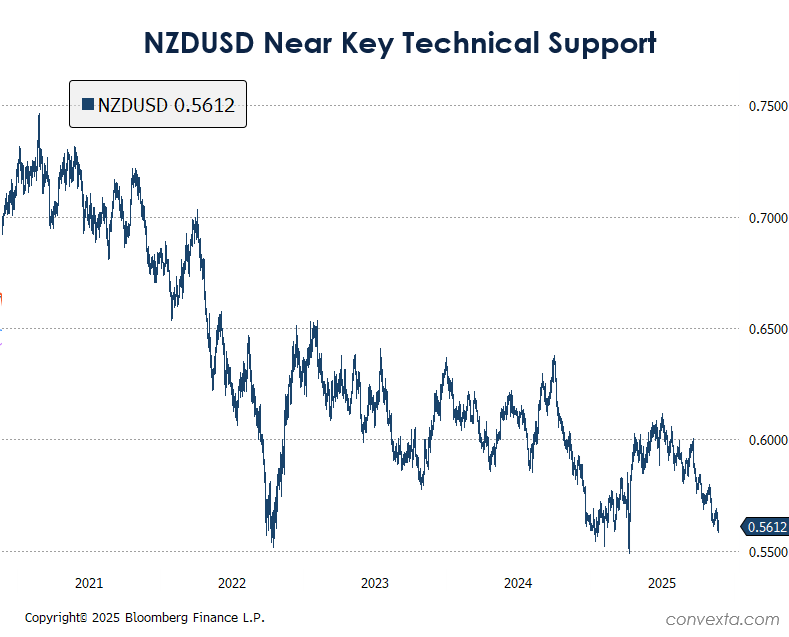

The silver lining is that the defensive trades were working as expected, albeit with size that didn’t provide a substantial gain during the volatile week. NZDUSD broke below 0.56 - a very significant level which opens 0.55 as the next target - a very strong support zone, previously touched in 2020 and 2022 (both very difficult years for risk assets).

Positioning and Trading Plan: Staying the Course

My portfolio positioning remains unapologetically bullish in the face of ongoing adversity. The 227% long allocation to equity markets and 131% long allocation to commodities reflect a high conviction in my Reflationary Growth theme, outlined originally in Positioning for Reflationary Growth on 20th of October.

Expected portfolio volatility increased to 44.6% during the week, solely due to the increasing underlying market volatility. With the risk budget fully deployed and technical signals softening at the margin, my general bias shifts to cutting risk on further weakness rather than buying the dips.

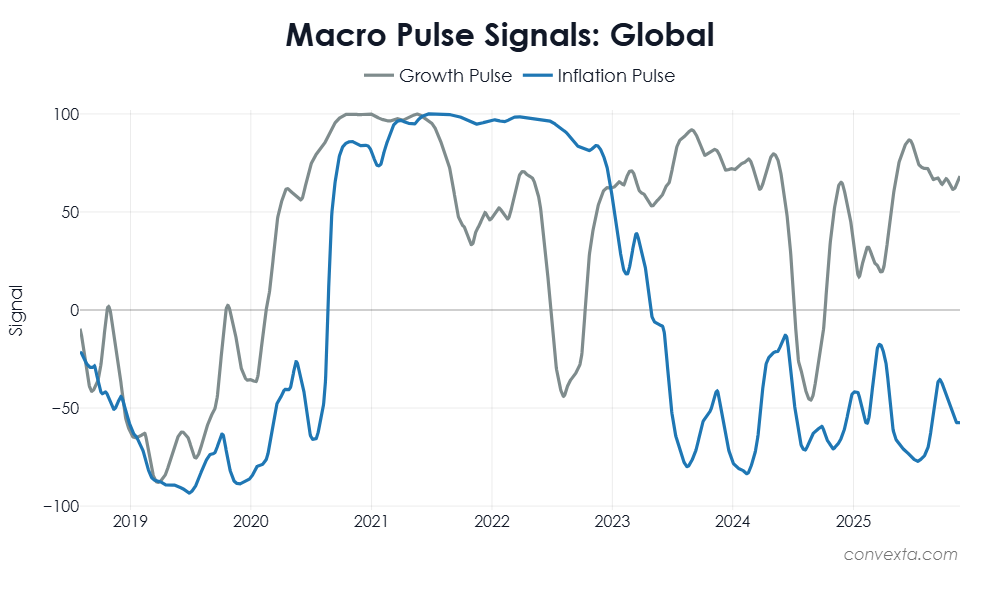

However, at this very moment, ongoing price weakness is strongly contradicted by improving fundamentals, so I see no strong reason to immediately de-risk. My Macro Pulse Indicators improved further during the week: global Growth Pulse moved higher, and the inflation pulse has remained unchanged since the last update, as shown below.

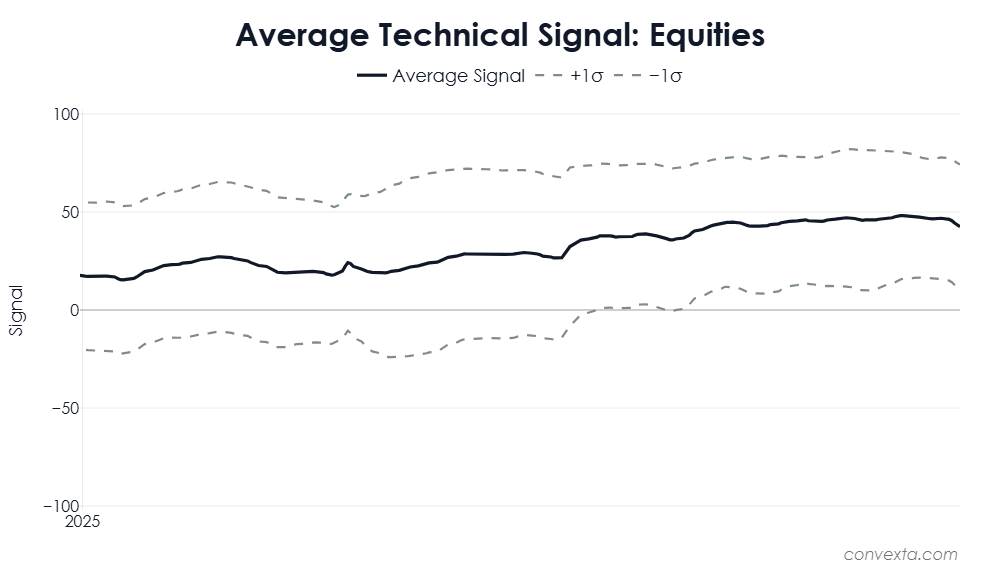

Technical signals for Equities have moved somewhat lower, mainly driven by slight trend deterioration, but remain at healthy bullish levels. CTA signals are nowhere near warning levels, and further buying is in the cards for a range of combinations of moderating volatility and firming prices from current levels.

The key adjustment relative to last week is the addition of 20% to short EURUSD and 20% to long USDJPY - as reported in my Live Trading Chat on Wednesday 19 November.

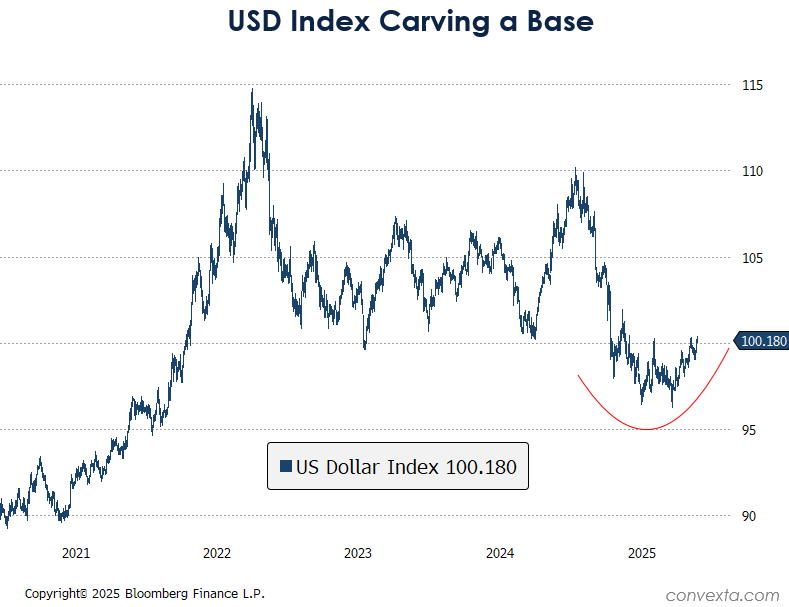

USD remains my defensive asset of choice in this environment, but as NZDUSD nears exhaustion and levels attractive for profit-taking, I am broadening my exposure to USD against the EUR. With my USDKRW long closed after BoK’s intervention warning, the nearest substitute is USDJPY, still supported by Japan’s policy mix outlined earlier.

The broad USD index looks like it’s forming a base. A break above 100.35 this week would be a clean confirmation, adding conviction to the long-USD stance.

Updated Trading Plan

Below is the summary of action points that I will be considering throughout the week

considerUSDJPY and/or Nikkei longs(completed on 19 November)explore potential short ideas in select commodities,

look for higher-conviction replacement for FTSE100 long / EURGBP short bundle

Add to JGB Shorts if signal firms and/or volatility normalises.

Consider de-risking on further weakness in signals or blanket increases in market volatility.

Key Catalysts This Week

Monday, Nov 24

Germany IFO business climate: an important read on euro-area growth momentum; softer sentiment would support the relative-UK view behind my EURGBP.

Singapore CPI: a contained print would reinforce the “safe, high-quality beta” angle for the long position in MSCI Singapore.

Taiwan unemployment: a secondary but useful signal for the tech/hardware cycle.

ECB President Christine Lagarde speaks.

Tuesday, Nov 25

Germany GDP, Hong Kong trade: GDP will shape the euro narrative, while Hong Kong trade is a read on China’s external demand and potential policy reaction.

US retail sales, PPI, Conference Board consumer confidence: key inputs for my “soft prices, softer labour” Fed narrative; weaker demand or benign PPI would nudge probabilities toward the December cut and support longs in equities and duration.

Alibaba earnings: a direct catalyst for the China Internet sleeve; margin commentary around AI and cloud spend may matter more than the headline beat/miss.

Asia Copper Week (Nov 25–27), LME positioning – sets the tone for copper and the broader base-metals complex that underpins JSE40.

Wednesday, Nov 26

Australia CPI: a cross-check on global goods and services inflation; another contained print would support the broader “disinflation with growth” backdrop.

New Zealand rate decision: a first-order catalyst for my NZDUSD short; a dovish cut or guidance reinforces the downside bias in NZD, while a more hawkish tone is the main risk.

Singapore industrial production: relevant for MSCI Singapore.

US durable goods and initial claims: demand and labour-market slack indicators

UK Autumn Budget: any surprise on tax or spending could move my FTSE100 and EURGBP positions.

Fed Beige Book: the qualitative backbone for the FOMC’s assessment ahead of December; evidence of softer activity or easing price pressures would be a clear positive for my non-consensus cut call.

Thursday, Nov 27

China industrial profits: read across to China Internet stocks + Metals and JSE40.

Eurozone consumer confidence: EURUSD and EURGBP catalyst.

Thanksgiving Day: thin liquidity and closed US markets; any macro or geopolitical surprise could have outsized impact on my positions once markets reopen.

Friday, Nov 28

South Africa trade balance: relevant for the JSE40 and indirectly for Gold/PGM demand, given the metals-heavy export basket.

Black Friday (US Holiday): real-time stress test of the US consumer.

China iron ore and SHFE inventory data, CFTC positioning: weekly flow and stock data that will colour the narrative around metals (Gold, Copper, PGMs), JSE40 miners, and my Diversifiers.

Eurozone CPI, GDP batch: Germany, Italy, France, Spain, Poland

Japan: Unemployment, Retail Sales, IP.

Sunday, Nov 30

China official PMIs (Nov): the big one for early next week: a key gauge of China’s growth pulse with direct implications for China Internet, JSE40, Copper, and the overall risk tone.

Disclaimer

We do not provide dealing, solicitation, or advisory services in futures or securities, and we do not offer asset management services. All our publications are made available to the public. Authors’ personal allocations and opinions are provided for educational purposes only, are not tailored to any specific reader, and do not constitute investment advice.

This article come at the perfect time! Your December Fed cut call feels so incredibly smart.